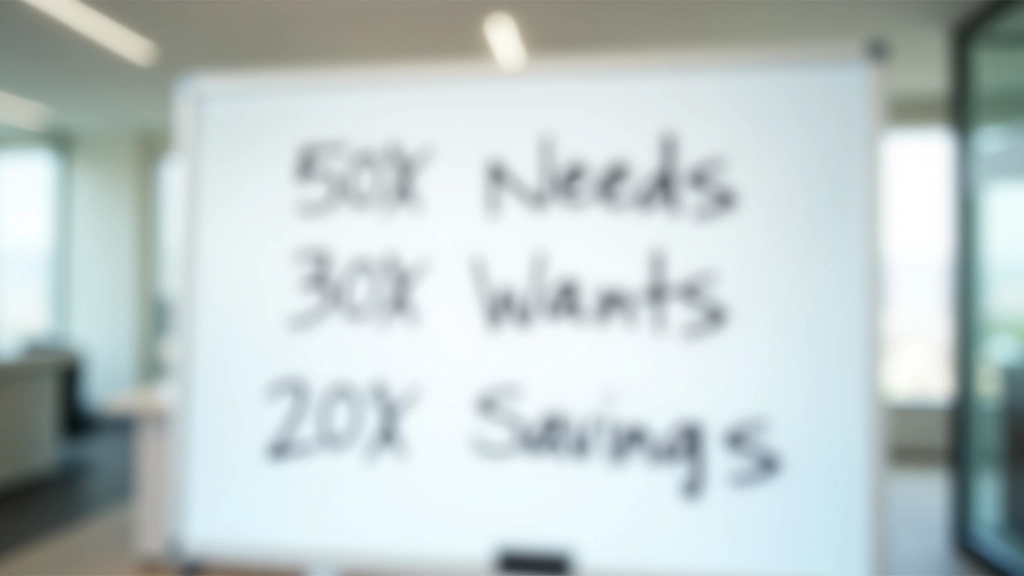

What Is the 50-30-20 Rule?

The 50-30-20 budget method is a straightforward approach to managing your money. It’s not complicated or rigid — it’s a framework you can actually stick to. Here’s how it works: split your after-tax income into three categories.

Fifty percent goes to needs. Thirty percent goes to wants. Twenty percent goes to savings and debt repayment. That’s it. No spreadsheets required (though they help). No apps tracking your every purchase. Just three buckets, three percentages, and a clearer picture of where your money’s going.

We like this method because it’s flexible. Your percentage might look different than someone else’s, and that’s fine. The point isn’t perfection — it’s clarity. You’ll know what you’re spending on essentials, what you’re allowing yourself to enjoy, and what you’re building for the future.